Investor Relations

Share

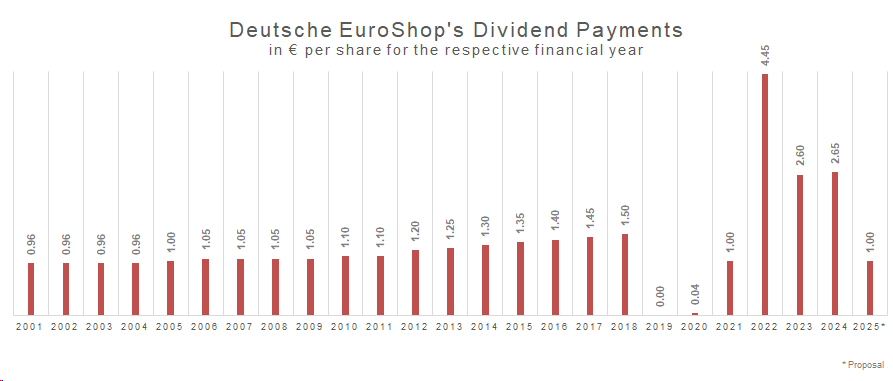

Deutsche EuroShop’s primary investment objective is to generate high surplus liquidity from long-term leases that we can pay out to our shareholders in the form of annual dividends. We want to enhance this so called free cash flow continuously and increase the dividend in the long-term.

Dividend development:

Dividends paid to shareholders domiciled in Germany are generally subject to income or corporation tax. Private investors are charged with the definitive withholding tax at a flat rate of 25% plus the solidarity surcharge as from 2009. Exceptions may be made under certain circumstances for dividend payments that are regarded as equity repayments for tax purposes (distributions from EK04 – equity class 04 – or, since 2001, from the tax-recognised contribution account). Deutsche EuroShop’s dividend partially fulfils this requirement. The dividend payment partially constitutes untaxable (i.e. tax-free) income for shareholders in accordance with section 20 (1) clause 1 sentence 3 of the Einkommensteuergesetz (German Income Tax Act).

However since 2009 these distributions are taxable due to the new legal status, as capital gains from securities are subject to tax if they are bought after 31 December 2008. In this case the acquisition costs are reduced by the dividends and lead to higher capital gains at the time of the disposal.

IR-Team

Nicolas Lissner (Senior Manager Investor & Public Relations, left) and Patrick Kiss (Head of Investor & Public Relations, right). More